There's a market inefficiency hiding in plain sight. PE firms with $50B+ AUM won't touch deals below $10M enterprise value — not because they don't want to, but because the economics don't work. And that's exactly where we play.

If you're an operator running a $3M–$8M EV business and you've been trying to get a clean exit, you've probably run into the same wall: institutional buyers want 90-day processes, earn-out negotiations that never end, and valuation math that makes you feel like you're the problem.

You're not the problem. The problem is their model.

The Math Nobody Talks About

A $50B AUM fund can't underwrite a $3M EV e-commerce brand — even when the IRR is 40%+. Here's why:

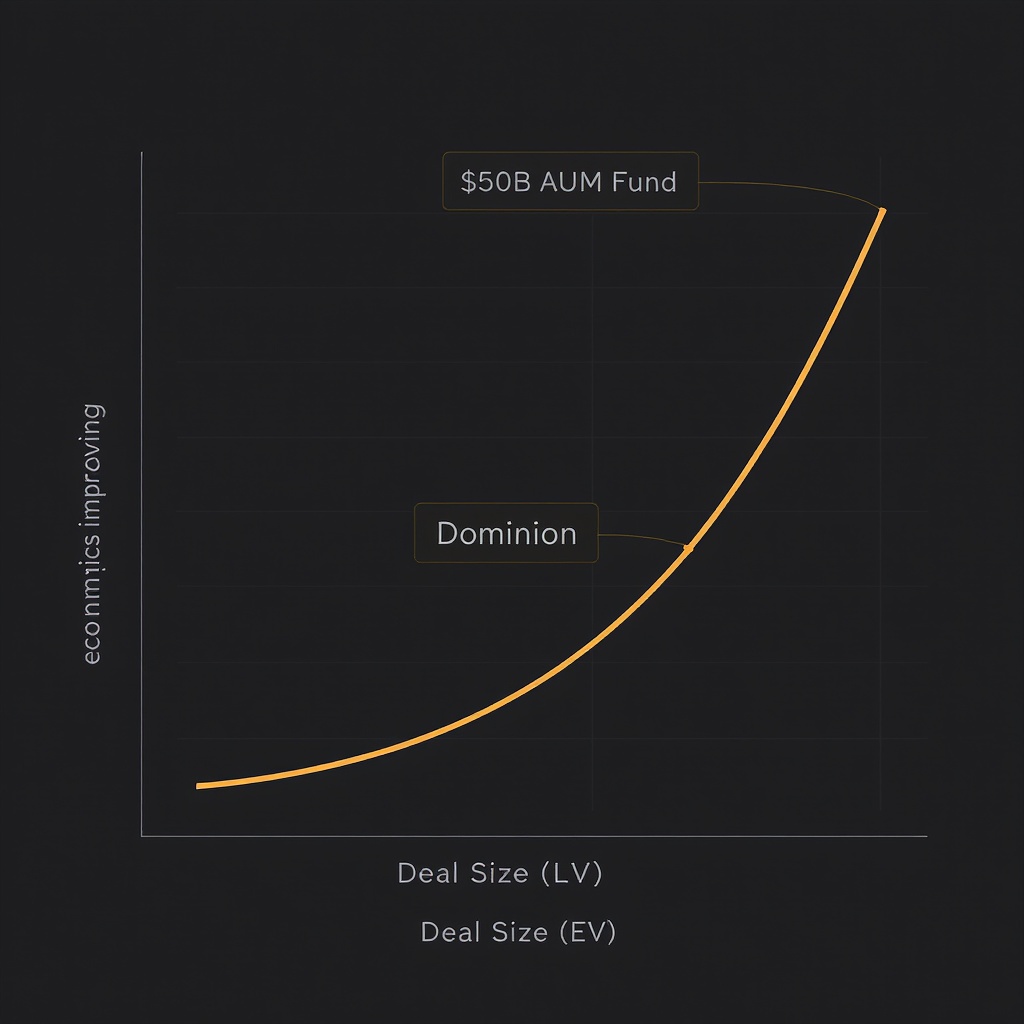

- Management fees don't cover due diligence costs. A $3M deal requires the same diligence work as a $30M deal — financial audit, market analysis, legal review, operational assessment. The time cost is fixed. The fee income isn't.

- IC overhead makes smaller deals dilutive to carry. Investment Committee decks, partner review cycles, legal sign-offs — these scale with deal count, not deal size. Running a $3M position through a full IC process actually costs the fund money on a carry basis.

- Portfolio concentration rules force the math. A $3M position in a $10B fund is noise. At that scale, the fund needs deal sizes that move the needle — and that means they can't efficiently own businesses that don't hit their minimum threshold.

Dominion's model is structurally different: no Investment Committee theater, thesis-driven underwriting, and lean ops that make economics work at $1M–$10M EV that a $50B fund literally cannot replicate.

We're not competing with PE firms. We're exploiting the structural gap they can't close — because their overhead model is the product, and it breaks at this deal size.

What Sub-$10M Operators Actually Want

In three years of running deals in this range, the same requests come up every time. Operators aren't looking for the highest price — they're looking for a clean process:

- Speed. Not 90-day processes. Operators who've been through institutional exits describe the timeline as "the worst part." They want a decision in weeks, not months.

- No earn-out games. Earn-outs sound reasonable in theory. In practice, they create adversarial dynamics where the seller has to perform for a buyer who's looking for reasons to reduce the final payment. Nobody wins.

- Operator continuity options. Founders who built the business want to know it continues. They care about their team, their customers, the product. Dominion offers operator continuity structures that let founders stay involved on their terms.

- Founder respect. This one's underrated. Most institutional buyers treat smaller operators as inferior. The same deck that gets a roll-up buyer excited makes them treat the founder like a transaction cost to be negotiated away. That's not how we work.

How Dominion Underwrites in 14 Days

We've compressed the standard M&A process from 90 days to 14. Here's how:

- AI-assisted screen. We run a fast thesis-fit assessment on every submission. Vertical, margin profile, customer concentration, market tailwinds — the screen filters for fit before a human looks at it. Operators get an answer within 48 hours of submission.

- Thesis-driven diligence. We don't run IC theater. Our diligence is structured around the specific risks in the vertical — supply chain for e-comm, churn drivers for SaaS, dealer inventory for MH, power contracts for data center. It's targeted, not generic.

- Lean ops = no overhead bloat. The same deal that costs a PE firm $150K in internal resources to underwrite costs us a fraction of that. The savings compound into better economics for everyone — including better entry prices for operators who need a fast, clean exit.

- 14-day decision timeline. From submission to LOI in 14 calendar days. That's the commitment. If you're running a parallel process with other buyers, Dominion's speed is the deciding factor — because by the time a traditional fund finishes their IC deck, we've already closed.

Where We're Active: The Four Verticals

We're not chasing every deal. We're thesis-specific in four verticals where sub-$10M businesses have structural advantages and where operator quality makes the difference between a good acquisition and a great one.

- E-Commerce. DTC brands and marketplace sellers with owned SKUs, repeat purchase rates, and supplier leverage. We're buying in a market where Amazon retail arbitrage is compressing margins — which means founders who built real brands are getting squeezed out. Good time to buy, better time to sell.

- AI/SaaS. Vertical software and AI tooling with recurring revenue, negative churn potential, and a sticky user base in infrastructure or ops workflows. Sub-$10M SaaS businesses with 80%+ gross margins are under-owned by institutional buyers who want $5M+ EBITDA floors. We don't need the floor — we need the trajectory.

- MH Dealerships. Manufactured home retailers in land-constrained markets. Low overhead, financing partnerships, inventory velocity. These businesses have been family-operated for generations — the owner approaching retirement is the deal, not the category. We've built a repeatable acquisition framework for this vertical.

- Data Center Infrastructure. Edge colocation, power infrastructure services, and hyperscale support businesses benefiting from AI buildout demand through 2030. AI isn't just software — it's physical infrastructure, and the companies building that infrastructure at the edge are exactly the kind of businesses that institutional buyers overlook because they don't fit the hyperscale mold.

"If you're an operator in this range and you've ever wondered what a clean exit looks like — no earn-out theater, no IC theater, just a decision and a check — run your numbers on our deal screen."— Joe Acosta, Founder & CEO, Dominion Capital Group Inc.

The inefficiency is structural. The big funds can't fix it without breaking their own model. That's our edge — and it's built into the architecture, not the pitch.